The pension mistakes costing you thousands before April

I've been helping business owners with their tax planning for years now. Every tax year end, I see the same patterns. People leave money on the table because they don't understand how pension contributions actually work. The deadline is 5th April 2026, and after that date, you'll lose opportunities that won't come back.

The tax system is designed to be complicated. That's not an accident. But pension tax relief is one area where the rules genuinely favour you if you know how to use them. The problem is that most people don't realise what they're missing until it's too late.

Here's what you need to know before the tax year runs out.

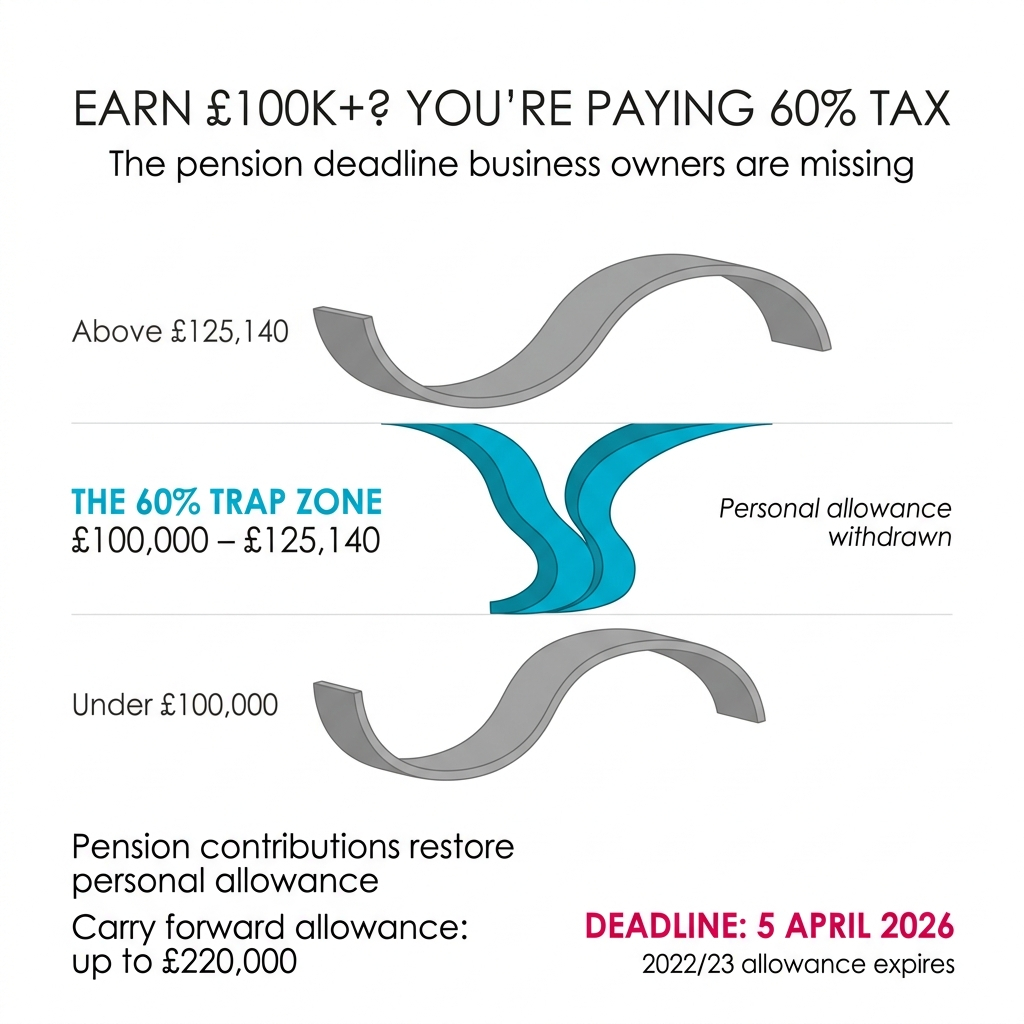

The 60% tax trap nobody warns you about

If you earn between £100,000 and £125,140, you're in a peculiar position. For every £2 you earn above £100,000, you lose £1 of your personal allowance. This creates an effective tax rate of 60% on that slice of income. Add National Insurance, and you're looking at 62%.

Let me break this down with actual numbers. Say you earn £110,000. That's £10,000 above the threshold. You'll pay £4,000 in higher-rate tax on that £10,000. But you'll also lose £5,000 of your personal allowance. That £5,000 is now taxable at 40%, costing you another £2,000. Of that £10,000, you keep £4,000. That's a 60% effective tax rate.

Most business owners I speak with don't realise they're in this trap. They see their income rising and assume they're doing well. They are doing well. But they're also handing over more to HMRC than they need to.

How pension contributions restore your personal allowance

There's a straightforward way to manage this. If you earn £110,000 and make a pension contribution of £10,000 through salary sacrifice, your adjusted net income falls to £100,000. This reinstates your full personal allowance. The effective rate of tax relief on that pension contribution becomes 60%.

This isn't a loophole. It's exactly how the system is designed to work. The government wants you to save for retirement. They've created tax incentives to encourage it. But you have to actually use them.

The annual allowance for 2025/26 is £60,000, or 100% of your UK earnings if that's lower. This covers all pension contributions, including what your employer puts in. For most of the businesses I work with, this is the limit they need to work within. Many aren't using it fully.

Carry forward rules you're probably not using

Here's where it gets interesting. You can carry forward unused pension allowances from the previous three tax years. Including the current tax year, that means you could contribute up to £220,000 in 2025/26 if you've not used your allowances in prior years.

I see this opportunity missed constantly. A client has a good year, receives a bonus, or sells part of their business. They've got a lump sum sitting there. They don't realise they can make a substantial pension contribution that goes far beyond the standard £60,000 annual limit.

The carry forward rules let you backfill those unused allowances. But there's a critical deadline. After 5th April 2026, any unused allowance from the 2022/23 tax year expires. It's use it or lose it. Once it's gone, it's gone.

How tax relief actually works in practice

When you contribute to a registered pension scheme, the government refunds the income tax you would have paid on that money. Pension contributions come from pre-tax income. A basic-rate taxpayer who wants to put £100 into their pension only sacrifices £80 of take-home pay. The other £20 comes from HMRC as tax relief.

If you pay 40% or 45% tax, you need to claim the additional relief yourself. Basic-rate relief happens automatically. But higher-rate taxpayers must claim the extra 20% or 25% through Self Assessment or a tax code adjustment. I see thousands of pounds in unclaimed relief every year because people don't realise they need to take this step.

This is money sitting on the table. You've already earned it. You're entitled to it. But if you don't claim it, HMRC keeps it.

The practical deadline that matters more than 5th April

The tax year ends on 5th April 2026. But that's not the deadline you should be working to. Most pension providers need payments to be received and processed before that date. Cheques can take up to five working days to clear. Electronic transfers need time to process and be credited to your account.

If you want contributions counted in the current tax year, make the transfer several days beforehand. Don't leave it until 5th April and hope it processes in time. I've seen contributions miss the tax year by a day because someone assumed same-day processing.

The safe approach is to aim for the end of March. That gives you buffer time for any processing delays, bank holidays, or administrative issues that might crop up.

What you should do right now

Look at your income for this tax year. If you're approaching or over £100,000, calculate whether you're in the 60% trap. Work out how much pension contribution would bring your adjusted net income back below the threshold.

Check your unused allowances from the previous three tax years. If you've not maximised your contributions in 2022/23, 2023/24, or 2024/25, you've got carry forward capacity. This is your last chance to use the 2022/23 allowance before it disappears.

If you're a higher-rate taxpayer and you've made pension contributions this year, check whether you've claimed all the relief you're entitled to. Basic-rate relief is automatic, but the additional relief isn't. You need to claim it.

Talk to someone who understands your specific situation. Every business is different. Your income structure, your company setup, your personal circumstances all affect what makes sense for you. Generic advice doesn't work when you're dealing with tax planning.

The opportunity that disappears on 6th April

I'm not going to promise this will transform your retirement or change your life. What I will tell you is that pension contributions are one of the most tax-efficient tools available to business owners. The relief is genuine. The savings are substantial. But the deadlines are real.

After 5th April 2026, the 2022/23 carry forward allowance is gone. You can't get it back. If you're in the 60% tax trap and you don't act, you'll keep paying that effective rate on income you could have sheltered. If you're entitled to higher-rate relief and you don't claim it, HMRC keeps that money.

The tax system is complicated because it's designed that way. But pension tax relief is one area where the rules work in your favour. You just have to use them before the deadline passes.

What's your current pension contribution strategy, and have you checked your carry forward position for this tax year?